PUBLISHED IN

Byline from Donald Sniezek,

Senior Technical Advisor

at alliantgroup,

Kathy Petronchak, Director

of IRS Practice & Procedure at

alliantgroup,

Matthew Beddingfield, Senior Associate

at Zerbe, Miller, Fingeret, Frank &

Jadav LLP

If you have any questions about this article, please send us a message.

The National Taxpayer Advocate (“NTA”) is required to submit a report to Congress by June 30 of every year pursuant to Code Sec. 7803(c)(B)(i). The National Taxpayer Advocate Objectives Report to Congress Fiscal Year 2024 (“mid-year report”) was issued on June 21, 2023, detailing how the Internal Revenue Service (“IRS”) has improved services since 2020 during the coronavirus disease 2019 (“COVID-19”) pandemic as well as objectives outlined by the Office of the Taxpayer Advocate for the upcoming fiscal year.

According to the mid-year report from the NTA Erin M. Collins, the “taxpayer experience vastly improved during the 2023 filing season,” adding that compared to last year’s filing season, the results were like “night and day.” While acknowledging these improvements, the mid-year report also noted that issues carried over, with the most noticeable being “delays in the processing of amended tax returns and taxpayer correspondence.”

The processing of original tax returns is the number one priority for the IRS each year and is monitored closely. In 2023, the status of unprocessed original paper tax returns (comparing weeks ending April 22 for both years) fell from 13,300,000 in 2022 to 2,600,000 in 2023. This was due to the IRS working through nearly all the backlogged individual returns from prior years before the filing season started. The NTA noted that this is a return to pre-pandemic levels.

While processing delays are usual for paper-filed returns since an IRS employee must keystroke each digit from a paper return into IRS systems, it was noted that as of April 22, 2023, there were still 2.6 million original individual and business paper income tax returns awaiting processing. In addition, there were 5.9 million individual and business electronic and paper-filed income tax returns that the IRS suspended for various reasons. These numbers have recently been updated and as of August 12, 2023, the IRS had 1.52 million unprocessed original individual returns for 2022 and prior years but 1.4 million of them require special handling or error correction.

Regarding amended returns, there was only a small reduction in the backlog from 2022 to 2023. The small reduction from 3.6 million to 3.4 million was primarily due to the IRS’s decision to prioritize phone services over paper processing. While systems have improved and allow for electronic filing of some amended returns, there is still manual processing, and the average time to process a Form 1040-X is seven months. These numbers have recently been updated, and as of August 19, 2023, the IRS had 1.04 million unprocessed amended 1040-X returns.

On the business side, Employee Retention Credit (“ERC”) claims on Form 941-X largely made up the processing delays. “The IRS believes that most ERC claims are legitimate, but a significant percentage are along the spectrum of very aggressive to fraudulent,” adding that by the end of May 2023, there was a backlog of approximately 800,000 ERC claims the IRS was working through, and more were arriving. These numbers have recently been updated, and as of August 24, 2023, the IRS had 1.1 million unprocessed Forms 941, and as of August 23, 2023, the IRS had approximately 556,000 Forms 941-X left to process.

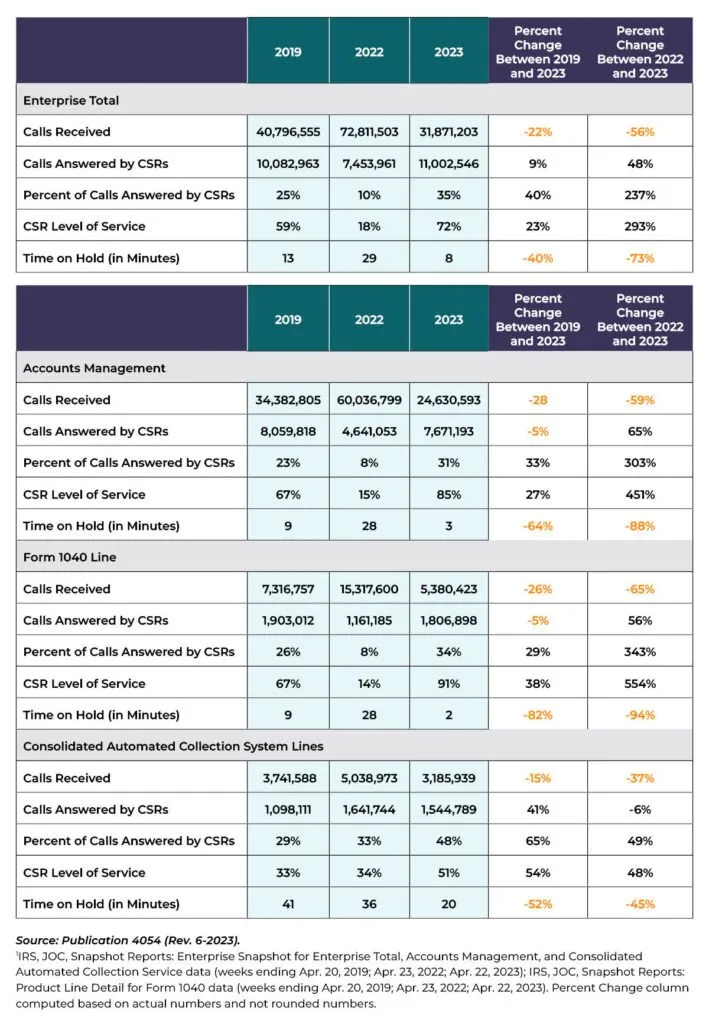

When it came to results for the IRS Enterprise Telephone Service, the agency reached the Treasury Department’s directed goal of 85 percent level of service (“LOS”); however,

that figure must be put into perspective. It is for the Accounts Management (“AM”) lines only and excludes 73 percent of the taxpayer calls received by the IRS. This computation excludes calls directed to compliance and other phone lines. Looking holistically, only 35 percent of the 32 million calls received were answered by an IRS employee. While the 85 percent LOS is great for those who got through to AM, certain phone lines did not experience this LOS. For example, the LOS for the “Automated Collection System” was only 51 percent, and there was an increased wait time for assistance.13 However, the LOS on the Refund Hotline and Practitioner Priority Service improved greatly in terms of LOS and average speed of answer. Additionally, modernization efforts continue on the phone lines by providing callback options and, most recently, voicebots.

Although the method of calculating LOS is confusing and may not reflect the taxpayer’s experience in seeking telephone assistance, Figure 2.4 (see below) has been provided to reflect changes before the pandemic and the last two filing seasons. This, along with Figure 2.3 in the mid-year report, provides useful information and paints a more complete picture of the taxpayer experience.

Although an additional 5,000 AM customer service representatives (CSRs) were hired, they perform two roles they answer telephone calls and they process taxpayer correspondence and cases, including amended returns.

While prioritizing the LOS benefited millions of taxpayers, it was only accomplished by creating greater delays in processing paper correspondence. Due to limitations of

antiquated technology and certain other factors, “CSRs assigned to answer the phones currently cannot perform other tasks while waiting for calls to come in. As a result,

CSRs were idle 34 percent of the time they were assigned to answer the phones, meaning they were neither assisting taxpayers on the phone nor processing amended tax

returns and taxpayer correspondence.”

Figure 2.5 in the mid-year Report, titled “Filing Season 2023, IRS Processing of Taxpayer Correspondence,” laid out the details of the five million pieces of taxpayer correspondence that need to be processed. Notably, the NTA stated that in “situations where the IRS needs a taxpayer response to move forward, but the IRS has not yet processed that response, its automated processes could take adverse action.”17 Due to the prioritization of LOS over paper processing, there was little progress made by the IRS in reducing these paper inventories resulting in potential harm to taxpayers.

The NTA also highlighted the myriad issues that a lack of technological upgrades has caused the IRS in recent years. Antiquated technologies have led to both processing and refund delays, particularly for paper processing. The NTA opined that relevant appropriations will not be enough to cover the technological needs of the agency.

“… to achieve and sustain transformational improvement over the longer term, the IRS must focus like a laser beam on IT. The IRS must give taxpayers robust online accounts that are comparable to accounts provided by banks and other financial institutions,” the report stated.

Along these lines, the NTA advocated for several improvements, including but not limited to:

- The possibility for all taxpayers to e-file tax returns,

- Limiting the number of rejected electronic tax returns,

- Faster relief for victims of identity theft, and

- The possibility for taxpayers to receive and submit responses to information requests electronically in all interactions with the agency.

These are all improvements that taxpayers would welcome. The Inflation Reduction Act (“IRA”) provides more funding for IT, and the IRS has identified priorities in a

Strategic Operating Plan released in April 2023.

In line with the NTA vision, the IRS announced in August 2023 its plans for a paperless processing initiative. The goal is that by filing season 2024 taxpayers will have an

option to go paperless for IRS correspondence and the processing of income tax returns. With IRA funding, the IRS is increasing the number of notices to which taxpayers can

respond online. All of this is welcome news to taxpayers.

The NTA also highlighted the Office of the Taxpayer Advocate upcoming fiscal year objectives. The key goals and activities are outlined for three areas: Systemic Advocacy Objectives, TAS Case Advocacy and Other Business Objectives, and TAS Research Objectives.

IRS TELEPHONE RESULTS, FILING SEASONS 2019, 2022, AND 2023, COMPARING WEEKS ENDING APRIL 20, 2019; APRIL 23, 2022; APRIL 22, 2023

Systemic Advocacy Objectives address areas to improve tax administration and systemic issues causing taxpayer burden or negative impact on taxpayer rights. TAS Case Advocacy and Other Business Objectives addresses how TAS will advance advocacy efforts in their casework. TAS Research Objectives focus on how IRS procedures impact taxpayers and taxpayer reactions to them. Twenty-six objectives are outlined in the mid-year report, of which there is something of interest for everyone.

Examples of systemic advocacy objectives listed by the NTA, in no particular order, included, but were not limited to, the following:

- Improving correspondence audit processes, taxpayer participation, and agreement and default rates;

- Implementing systemic first-time penalty abatements but allowing reasonable cause;

- Eliminating the systemic assessment and offering First Time Abatement waiver for international information return penalties;

- Modernizing IRS paper processing procedures;

- Improving taxpayer access to telephone and face-to-face assistance;

- Increasing access to taxpayer accounts through online services; and

- Improving the staffing and culture of the IRS Independent Office of Appeals.

Conclusion

The NTA has again provided a window into the filing season and put things into perspective for taxpayers and practitioners who do not always agree with the public comments being made. There has been progress at the IRS in answering phones, with much still to be done to ensure timely responses and transparency for taxpayers. Let us hope the IRS continues its progress and goes into the 2023 filing season even better prepared.

An Update on Alternative Dispute Resolution

In other news, the Government Accountability Office (“GAO”) recently released its report on its assessment of Internal Revenue Service alternative dispute resolution (“ADR”) programs. These programs provide mediation to expedite resolution and avoid lengthy traditional appeals and litigation processes.24 The report found that “the use of these programs fell by 65 percent between Fiscal Years 2013 and 2022, and the IRS does not have enough data to understand why. For instance, the IRS does not collect data on how often it rejects taxpayers’ requests to use these programs. It also does not collect data on the results of using some of these programs—such as the actual time and costs involved.”

The GAO made recommendations to improve how the IRS manages its ADR programs, including that the IRS should improve its ADR data collection, establish clear program objectives, analyze data to better achieve ADR’s benefits, monitor taxpayers’ experience to assess ways to improve it, and establish responsibilities and tasks for managing ADR programs. The IRS generally agreed with the recommendations.

On July 27, 2023, the IRS Independent Office of Appeals invited the public to provide input on ways to improve alternative dispute resolution options. Andy Keyso, Chief Independent Office of Appeals, noted that “the IRS is greatly interested in examining ways to help to reduce the time, costs and administrative burden for taxpayers and the government in resolving tax disputes.”

Conclusion

Possibly with the GAO recommendations and the Chief Independent Office of Appeals soliciting feedback on these valuable programs, changes will take place at the IRS. There is not much information on why these are not being utilized, but what is apparent is that they provide an opportunity for both the taxpayer and the IRS to reach an agreement on issues at a much earlier stage than currently exists.

Featured Leadership

Kathy Petronchak is the Director of IRS Practices and Procedure at alliantgroup and is part of the alliantnational group in Washington, DC. In this role, she serves as an invaluable resource on a wide range of issues related to IRS procedures, such as foreign bank account reporting, alternative dispute resolution; statute of limitations; account problems, collection issues, and penalty issues. She is currently the Chair of the AICPA IRS Advocacy & Relations Committee and has served on various committees the past 11 years.

Donald Sniezek joined alliantgroup from the IRS, where he spent more than 34 years of his career, holding a number of Senior Executive Service positions culminating in appointment as Director of Examination Headquarters for the Small Business and Self-Employed (SBSE) Division. He uses his years of experience at the IRS to assist alliantgroup’s clients as a technical advisor and ambassador for U.S. small and medium sized businesses (SMBs).