If you have any questions about this article, please send us a message.

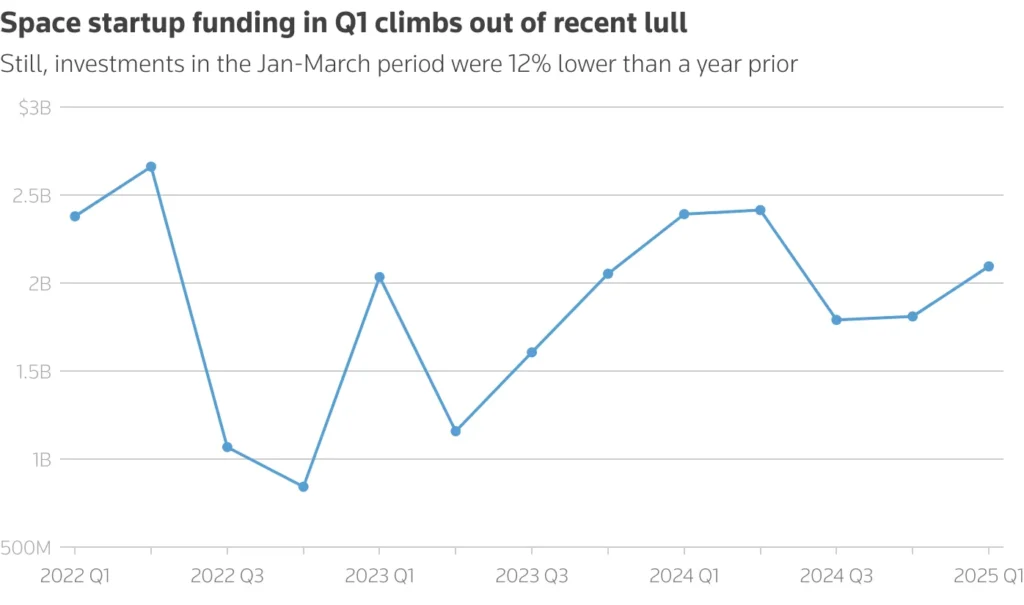

Source: Seraphim Space

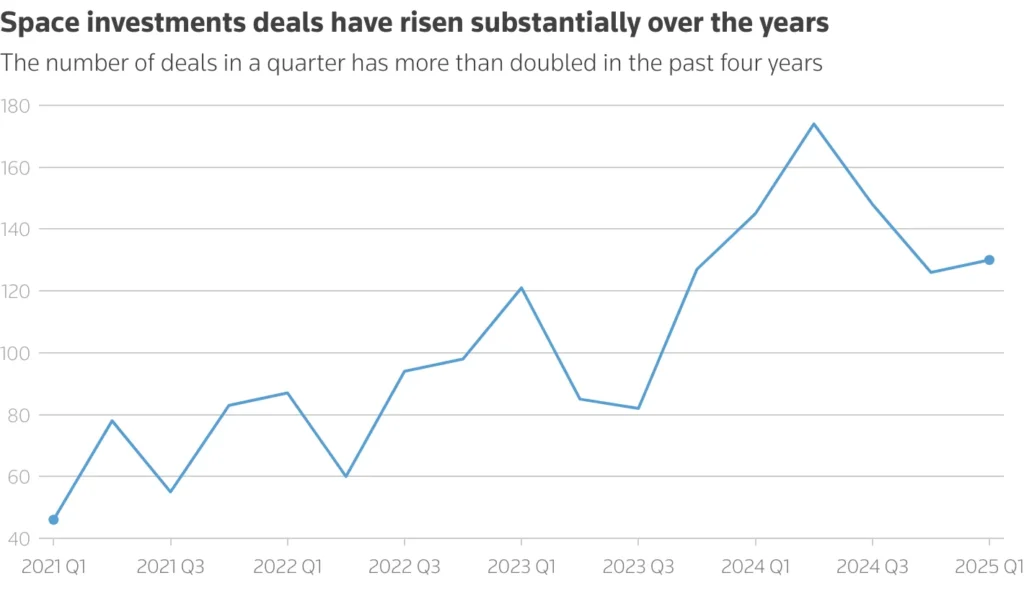

Source: Seraphim Space

While Zerbe welcomes the expansions to Code Sec. 179D, he said that the labor requirements are “a real dampener” for some claimants and limit businesses’ ability to “take full advantage of the tax benefit.” He explained that complying with the reporting aspects of the requirements may prove difficult for some contractors or subcontractors that “won’t know what the story is for all the workers onsite” in terms of wage and apprenticeship hours.

“We’re expecting you’ll have a significant number of companies that won’t be able to meet” those thresholds,” said Zerbe, who previously served as senior counsel and tax counsel for former Senate Finance Committee Chair Chuck Grassley, Republican of Iowa, from 2001-2008 and is now a partner at Zerbe, Miller, Fingeret, Frank & Jadav LLP. Variation in state laws may also muddy the ease in which companies can report necessary worker information, such as if a state is a so-called right-to-work state. Zerbe said “it’s a little bit surprising because [the Inflation Reduction Act] was put in place because of concerns about climate and energy efficiency. It’s pretty unheard of … having these kinds of labor requirement provisions put in place.”

Despite Zerbe’s reservations toward those guardrails under the inflation bill, he was pleased that an alliantgroup client secured a win in the U.S. Tax Court in Johnson v. Comm. (160 T.C. No. 2) late January. Taxpayer Edwards 4 Engineering, an S corporation represented by partners at Zerbe’s firm, prevailed against the IRS’ disallowance of their deduction for HVAC work done on a VA hospital in 2013. The IRS had brought numerous technical objections to court as to why the deduction should not have been allowed, but the Tax Court ruled that Edwards followed the requirements set forth in the IRS’ own guidance (Notice 2008-40).

Zerbe said it was “heartening” that the Tax Court “took a common sense, practical view” of a real-world application of how the Code Sec. 179D deduction is claimed. He said that the IRS took a “ticky-tack” position in their arguments, and that overcoming IRS scrutiny when claiming Code Sec. 179D can feel like “more of a game” opposed to good faith taxpayers receiving benefits as statutorily intended.

“Getting those [arguments] knocked out should hopefully clear the deck in a lot of ways and give designers, particularly contractors, greater confidence going forward,” said Zerbe, calling the decision an “important win for folks in this field.”

About the Author

Dr. Robert Ambrose received his Ph.D. from the University of Texas at Austin in Mechanical Engineering and received his M.S. and B.S. degrees from Washington University in St. Louis. Ambrose joined the faculty of Texas A&M and accepted the J. Mike Walker Chair in Mechanical Engineering in August 2021. Also in August of 2021, Dr. Ambrose retired from NASA, where he served in the Senior Executive Service as the Chief of the Software, Robotics and Simulation Division at NASA’s Johnson Space Center in Houston, Texas. He continues to serve as the Director for Space and Robotics at the Bush Combat Development Complex and his research interests are in space systems for defense, security and commercial applications, as well as robotics and autonomous systems for helping humans on Earth.